Category | Quality Management

Last Updated On 01/06/2026

Did you know that nearly 30% of audit failures globally are linked to a lack of professional skepticism? In a world where financial fraud, compliance gaps, and data manipulation are becoming increasingly sophisticated, one trait separates an average auditor from an exceptional one—auditor professional skepticism.

But here’s the real question:

Are auditors truly questioning what they see, or just validating what they expect?

Are auditors truly questioning what they see, or just validating what they expect? For certification candidates, this distinction is critical—not just for passing exams, but for applying auditing principles in real-world scenarios. This isn’t just a best practice; it is a core requirement of ISA 200 (International Standard on Auditing) and ISO 19011:2018, which mandate that auditors plan and perform audits with an attitude of professional skepticism.

Whether you're an aspiring auditor, a compliance professional, or someone preparing for certification, understanding auditor professional skepticism is no longer optional—it’s essential.

Let’s break it down step by step.

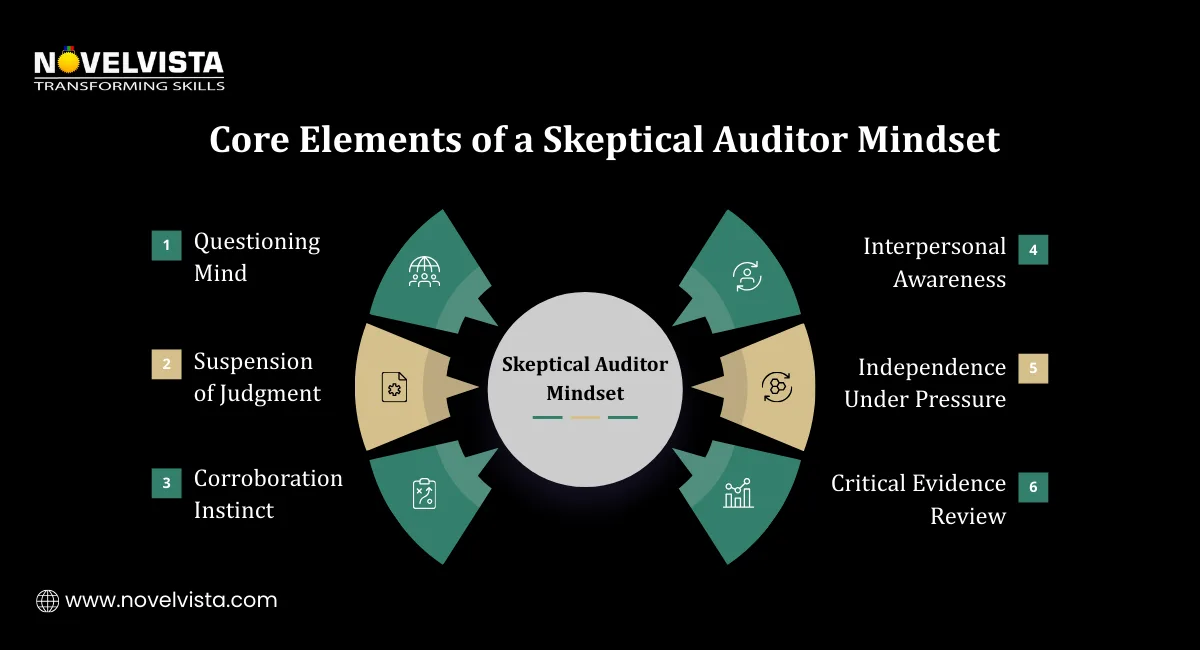

At its core, auditor professional skepticism is a mindset centered on questioning, critical thinking, and not accepting information at face value. It doesn’t imply distrust; rather, it reflects a balanced and neutral approach while evaluating audit evidence. This mindset is characterized by a questioning attitude, a keen alertness to inconsistencies, and the ability to critically assess information before drawing conclusions. In today’s auditing environment, where automation and complex data systems are increasingly common, this approach has become essential. Auditors are expected to move beyond routine checklists and actively analyze and interpret findings. Without this mindset, there is a higher risk of missing fraud indicators, overlooking errors, or accepting misleading data, ultimately compromising the quality and reliability of the audit.

Skepticism is not a binary switch it exists on a spectrum. At one end is neutrality, where auditors assume neither honesty nor dishonesty, and at the other is presumptive doubt, where there is a heightened awareness of potential misstatements. In high-risk areas, auditors are expected to shift closer to presumptive doubt, applying deeper scrutiny and more rigorous verification to ensure audit accuracy.

Audit objectivity is the foundation upon which professional skepticism is built. Without objectivity, skepticism becomes biased or worse, ineffective.

It refers to the ability to remain impartial, unbiased, and independent during an audit, regardless of external pressures or personal judgments. This means evaluating all information fairly, without letting assumptions, relationships, or prior experiences influence decisions. An objective approach ensures that findings are based solely on facts and evidence rather than opinions. Maintaining this level of independence is essential for delivering accurate, credible, and trustworthy audit outcomes.

Imagine an auditor who assumes that a long-term client is always compliant. That assumption directly conflicts with auditor professional skepticism and weakens the audit process.

Objectivity ensures that skepticism is applied fairly not selectively.

Together, audit objectivity and skepticism create a balanced and reliable auditing approach.

A strong auditor mindset goes beyond ticking boxes. It’s about digging deeper, asking “why,” and validating every claim.

For example, if financial records show consistent growth, a skeptical auditor doesn’t just accept it they investigate:

This is where auditor professional skepticism truly comes into play.

An auditor notices slight discrepancies in inventory records. Instead of ignoring them, they investigate further, uncovering a larger issue of stock mismanagement.

That’s the power of the right auditor mindset.

No audit is complete without verifying audit evidence, as this step ensures that all findings are backed by reliable and accurate information. This is where skepticism moves from theory into practical application, requiring auditors to actively question and validate the data they receive. Instead of relying solely on provided documents, auditors must cross-check sources, assess authenticity, and look for inconsistencies. This process strengthens the credibility of the audit and ensures that conclusions are based on solid, defensible evidence.

Audit evidence includes:

Auditor professional skepticism ensures that evidence is not just collected but critically evaluated.

Always ask:

“Is this evidence sufficient and reliable?”

Ethics play a huge role in auditing, and the IRCA code of conduct provides a strong framework for auditors to follow. It outlines key principles such as integrity, objectivity, and professional competence, ensuring auditors act responsibly in every situation. By adhering to these guidelines, auditors can maintain independence and build trust with stakeholders. This ethical foundation also supports consistent decision-making, especially in complex or high-pressure audit scenarios.

The IRCA code of conduct reinforces the importance of maintaining audit objectivity and applying auditor professional skepticism consistently.

An auditor guided by ethical standards is more likely to question irregularities and avoid biased judgments.

Despite its importance, applying auditor professional skepticism isn’t always easy.

1. Organizational Pressure

Auditors may feel pressured to meet deadlines or satisfy clients, leading to compromised skepticism.

2. Time Constraints

Limited time can result in superficial checks rather than thorough verification.

3. Over-Reliance on Systems

Automated systems can create a false sense of accuracy, reducing the need for questioning.

4. Familiarity Threat

Long-term relationships with clients may reduce audit objectivity.

5. Cognitive Bias

Specifically, confirmation bias where an auditor subconsciously favors information that supports their existing beliefs or the client’s initial claims, potentially overlooking contradictory evidence.

Avoiding common ISO 9001 Audit Mistakes is essential to ensure accurate findings, maintain compliance, and improve overall audit effectiveness.

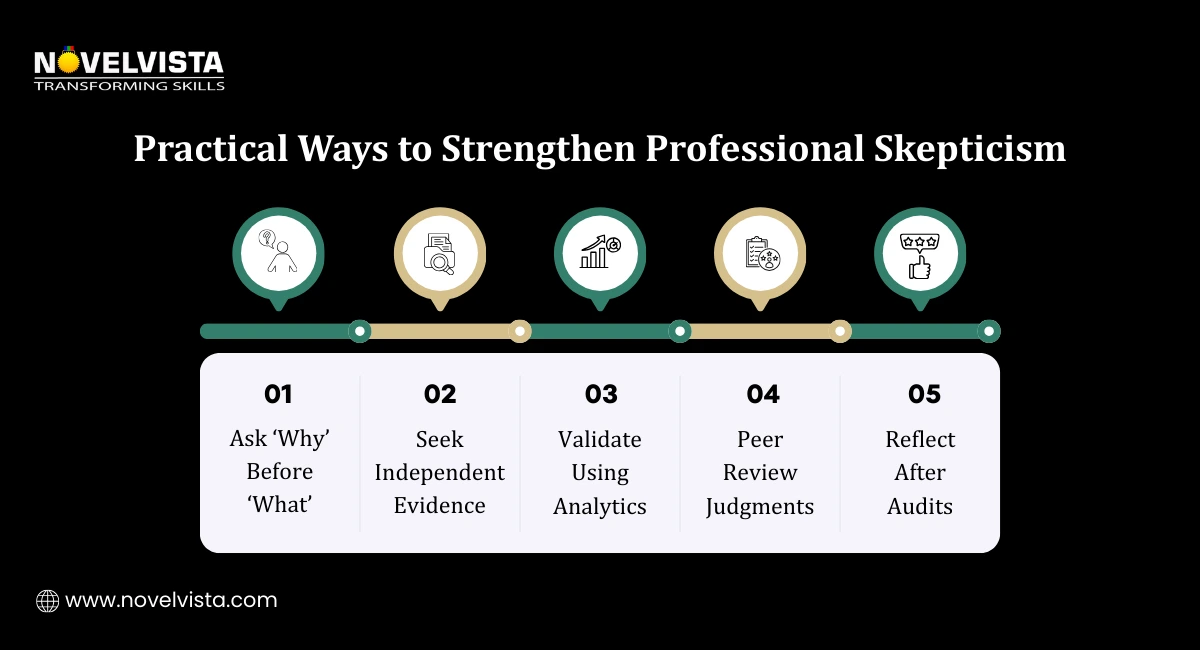

Improving auditor professional skepticism requires conscious effort and continuous learning.

Ask the Right Questions

Don’t just accept answers at face value—dig deeper into the details. Ask follow-up questions to understand the “why” behind the data and responses. This helps uncover hidden risks, inconsistencies, or gaps that may not be immediately visible.

Use Data Analytics

Leverage modern data analytics tools to go beyond manual checks and identify unusual patterns or anomalies. These tools can help auditors analyze large datasets efficiently and highlight areas that require closer examination.

Maintain Independence

Avoid conflicts of interest and ensure your judgments are not influenced by external pressures or personal relationships. Maintaining independence is key to preserving audit objectivity and ensuring fair, unbiased conclusions.

Continuous Training

Stay updated with evolving audit standards, tools, and frameworks, including the IRCA code of conduct. Ongoing learning helps sharpen your skills and keeps you aligned with industry best practices.

Document Your Judgments

Clearly document your observations, decisions, and the reasoning behind them. Proper documentation not only supports your conclusions but also enhances transparency and accountability during reviews or audits.

Adopt a mindset of “Verify, then Trust” a simple yet powerful approach.

In today’s rapidly evolving audit landscape, auditor professional skepticism is no longer a “nice-to-have” it’s the foundation of every high-quality audit. It empowers auditors to move beyond assumptions, uphold audit objectivity, and ensure every conclusion is backed by thoroughly verifying audit evidence.

As organizations grow more complex and risks become less visible, the ability to question, analyze, and challenge information becomes a true differentiator. Auditors who cultivate a strong auditor mindset and align with ethical principles like the IRCA code of conduct don’t just perform audits, they build credibility, trust, and long-term value.

Ultimately, the future of auditing belongs to professionals who don’t just accept information, but rigorously test it, validate it, and stand confidently behind it.

Ready to strengthen your auditing expertise and master auditor professional skepticism in real-world scenarios?

Join NovelVista’s ISO 9001 Lead Auditor Certification Training and gain hands-on auditing skills, practical insights into quality management systems, and globally recognized credentials. Designed for quality professionals, auditors, and compliance leaders, this course equips you with the ability to plan, conduct, and manage audits with confidence while applying principles like audit objectivity and verifying audit evidence effectively.

Take the next step in your auditing journey and become a confident, industry-ready lead auditor today!

Author Details

Course Related To This blog

ISO 9001:2015 Lead Auditor Training and Certification

Confused About Certification?

Get Free Consultation Call

Stay ahead of the curve by tapping into the latest emerging trends and transforming your subscription into a powerful resource. Maximize every feature, unlock exclusive benefits, and ensure you're always one step ahead in your journey to success.